High interest debt can quickly become difficult to manage, especially when multiple credit cards or loans are involved. Debt consolidation loans provide a solution by combining several debts into a single loan with one monthly payment. This strategy can simplify financial management and potentially reduce the total interest paid over time.

Debt consolidation is commonly used by individuals who want to pay off credit card balances, personal loans, or other high interest obligations more efficiently.

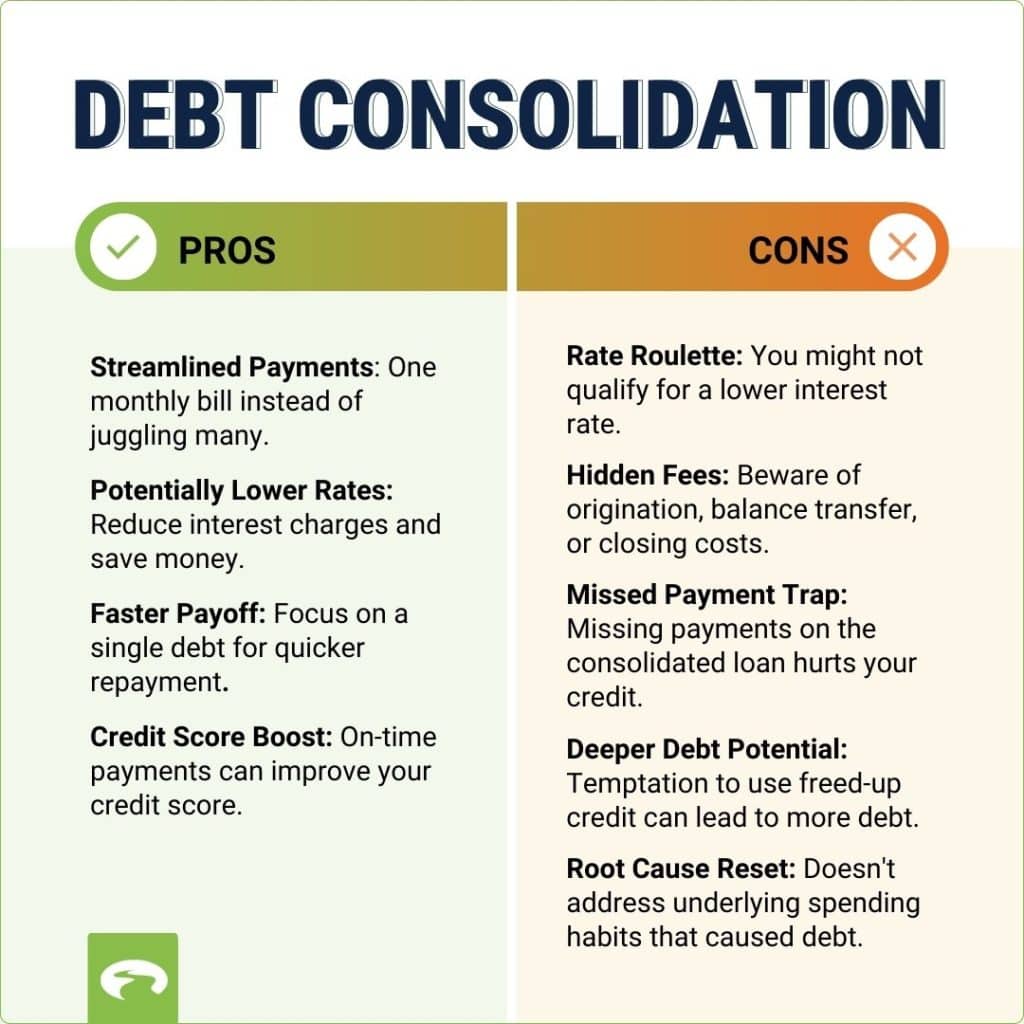

What Is a Debt Consolidation Loan

A debt consolidation loan is a personal loan used to pay off multiple existing debts. After receiving the loan, the borrower uses the funds to repay outstanding balances on credit cards or other loans.

Once the debts are consolidated, the borrower only needs to make a single monthly payment toward the new loan. This simplifies the repayment process and often provides a lower interest rate than credit cards.

Debt consolidation loans usually have fixed interest rates and structured repayment terms, making budgeting easier for borrowers.

Benefits of Debt Consolidation

One of the main advantages of debt consolidation is lower interest rates. Credit cards often have very high annual percentage rates, while personal loans typically offer more competitive rates.

Another benefit is simplified payments. Managing multiple debts can be confusing and stressful, but consolidation allows borrowers to track a single payment.

Debt consolidation may also improve credit scores over time if borrowers make consistent payments and reduce overall credit utilization.

Additionally, structured repayment plans can help borrowers become debt-free within a predictable timeframe.

SoFi Personal Loans

SoFi is a well-known financial technology company that offers personal loans designed for debt consolidation. The platform provides competitive interest rates and flexible repayment terms.

SoFi loans can be used to pay off high interest credit card balances and other debts, helping borrowers reduce their financial burden.

Key Features:

- Competitive interest rates

- No prepayment penalties

- Flexible loan terms

- Additional financial planning tools

LightStream Personal Loans

LightStream, a division of Truist Bank, offers personal loans with low interest rates for qualified borrowers. These loans are commonly used for debt consolidation because of their favorable terms.

LightStream focuses on borrowers with strong credit profiles but provides competitive rates that can significantly reduce interest costs.

Key Features:

- Low interest rates for qualified applicants

- No fees or prepayment penalties

- Loan amounts up to $100,000

- Flexible repayment options

Discover Personal Loans

Discover offers personal loans that are frequently used for consolidating high interest debt. The platform provides straightforward loan terms and no origination fees.

Borrowers can apply online and receive quick decisions regarding loan approval.

Key Features:

- No origination fees

- Fixed monthly payments

- Competitive interest rates

- Simple online application process

Upgrade Personal Loans

Upgrade is an online lender that offers personal loans designed for borrowers with a wide range of credit scores. The platform provides flexible loan options that help individuals consolidate credit card debt and other financial obligations.

Upgrade also offers financial tools that help borrowers manage their credit more effectively.

Key Features:

- Loans for various credit profiles

- Flexible repayment terms

- Fast online approval process

- Credit monitoring tools

How to Qualify for a Debt Consolidation Loan

Lenders evaluate several factors before approving consolidation loans. Credit score is one of the most important factors because it reflects the borrower’s history of repaying debts.

Income stability is another important consideration. Lenders want to ensure that borrowers have sufficient income to manage monthly payments.

Debt-to-income ratio is also reviewed. This ratio compares total monthly debt payments to income and helps lenders evaluate financial risk.

Borrowers with lower debt ratios and stable employment often receive better loan offers.

Tips for Successful Debt Consolidation

Before applying for a consolidation loan, borrowers should review their current debts and calculate the total amount owed. Understanding existing interest rates helps determine whether consolidation will provide meaningful savings.

Comparing offers from multiple lenders is also important. Interest rates, fees, and repayment terms can vary significantly.

Borrowers should also avoid accumulating new debt while repaying the consolidation loan. Continuing to use credit cards heavily may lead to even greater financial problems.

Creating a budget and following a structured repayment plan can help ensure successful debt elimination.

Risks of Debt Consolidation

Although consolidation can simplify debt repayment, it may not always solve financial problems if spending habits do not change.

Extending loan terms may reduce monthly payments but could increase the total interest paid over time.

Some lenders may also charge origination fees or other charges that increase the total cost of the loan.

Borrowers should carefully review loan agreements and ensure that the new loan offers genuine financial benefits.

Debt consolidation loans can provide a practical solution for individuals struggling with high interest debt. By combining multiple debts into a single loan with a lower interest rate, borrowers can simplify payments and potentially reduce overall financial costs. Lenders such as SoFi, LightStream, Discover, and Upgrade offer competitive loan options designed for debt consolidation. With careful planning and responsible financial habits, borrowers can use consolidation loans as an effective strategy for achieving long-term financial stability.