Access to capital is one of the most important factors for business growth. Whether a company needs funds for expansion, inventory, equipment, or operational expenses, a business loan can provide the financial support required to scale operations. However, many entrepreneurs struggle with the loan approval process because lenders evaluate several financial factors before providing funding.

Understanding how business loans work and preparing properly can significantly increase the chances of getting approved quickly.

Understand the Types of Business Loans

Before applying for funding, it is important to understand the different types of business loans available. Each type of loan serves different business needs.

Term loans are the most common type of business financing. Businesses receive a lump sum amount and repay it in fixed monthly installments over a specific period.

Business lines of credit provide flexible funding that allows companies to borrow money as needed up to a certain limit. Interest is only charged on the amount that is used.

Equipment financing is specifically designed for purchasing business equipment or machinery. The equipment itself often serves as collateral for the loan.

SBA loans are government-backed loans designed to help small businesses access affordable financing with favorable terms.

Improve Your Business Credit Score

Business credit scores play a major role in loan approval decisions. Lenders evaluate credit reports to determine whether a business has a strong history of repaying debts.

A higher credit score indicates lower risk to lenders, which increases the chances of loan approval and better interest rates.

Business owners can improve their credit scores by paying bills on time, reducing outstanding debt, and maintaining a good relationship with vendors and creditors.

Separating personal and business finances also helps establish stronger business credit profiles.

Prepare a Strong Business Plan

A well-prepared business plan demonstrates to lenders that the company has a clear strategy for growth and financial management.

Business plans typically include information about the company’s products or services, target market, competitive advantages, and financial projections.

Lenders want to see how the borrowed funds will be used and how the business plans to generate revenue to repay the loan.

Providing clear financial forecasts and realistic growth strategies increases lender confidence.

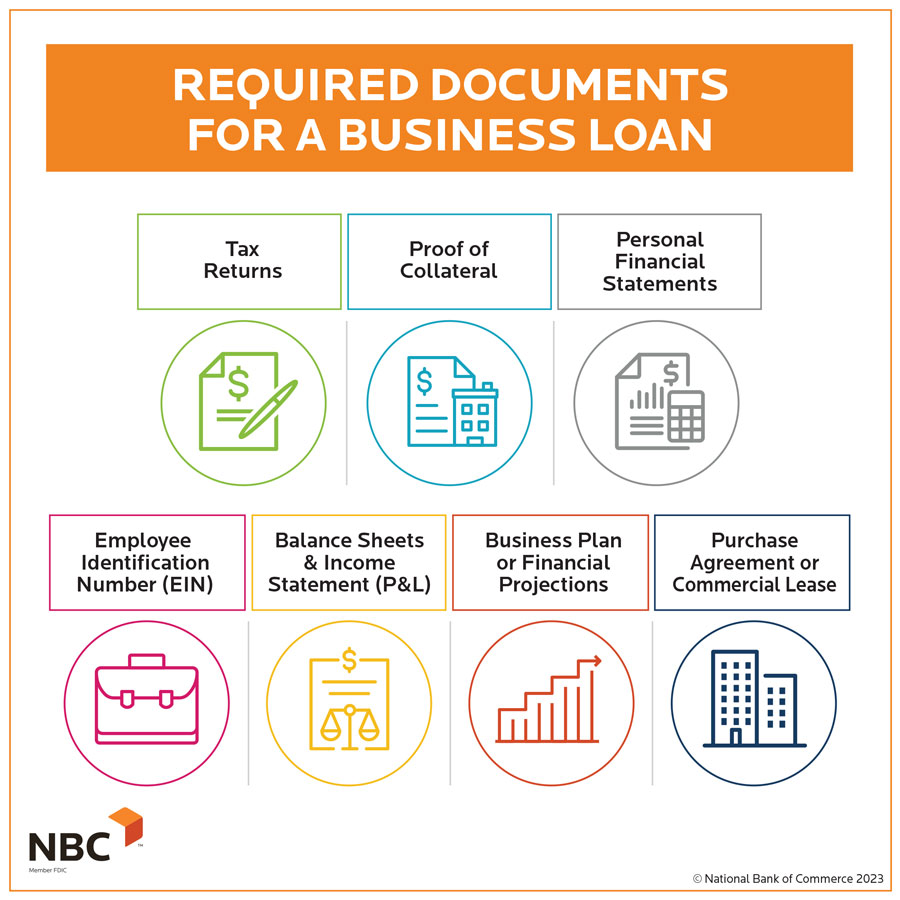

Organize Financial Documents

Most lenders require several financial documents before approving business loans. Preparing these documents in advance can speed up the approval process.

Common documents requested by lenders include bank statements, tax returns, profit and loss statements, and balance sheets.

Business owners may also need to provide identification documents, business licenses, and legal registration certificates.

Having these documents ready ensures that the application process moves smoothly without unnecessary delays.

Maintain Consistent Revenue

Lenders prefer businesses that demonstrate stable and predictable revenue. Companies with consistent income are considered less risky because they are more likely to repay loans on time.

Maintaining accurate financial records helps demonstrate the company’s financial health.

Businesses that show steady revenue growth are often more attractive to lenders and may qualify for larger loan amounts.

Reduce Existing Debt

Businesses with excessive debt may struggle to get approved for additional loans. Lenders evaluate the debt-to-income ratio to determine whether the company can handle additional financial obligations.

Reducing existing debts before applying for new financing can improve approval chances.

Paying off smaller loans or credit balances may help improve the overall financial profile of the business.

Choose the Right Lender

Different lenders have different requirements and approval processes. Traditional banks often have strict lending criteria, while online lenders may provide faster approvals and more flexible eligibility requirements.

Credit unions and community lenders may also offer favorable loan terms for small businesses.

Researching multiple lenders and comparing loan offers helps businesses find financing options that best match their needs.

Consider Collateral

Some business loans require collateral to reduce the lender’s risk. Collateral may include property, equipment, inventory, or other valuable assets owned by the business.

Providing collateral can improve approval chances and may help secure lower interest rates.

However, business owners should carefully consider the risks involved because failure to repay the loan could result in losing the pledged assets.

Apply for the Right Loan Amount

Requesting a realistic loan amount increases the chances of approval. Businesses should carefully calculate how much funding they actually need rather than applying for excessively large loans.

Lenders often evaluate whether the requested amount aligns with the company’s financial capacity and business plan.

Applying for manageable loan amounts can lead to faster approvals and more favorable loan terms.

Build a Relationship With Lenders

Establishing strong relationships with financial institutions can make the loan process easier. Businesses that maintain accounts with banks or lenders may have better access to financing opportunities.

Consistent communication with lenders and responsible financial management can build trust and increase the likelihood of loan approvals in the future.

Banks often prefer lending to businesses that demonstrate long-term stability and financial responsibility.

Getting approved for a business loan quickly requires careful preparation and strong financial management. Business owners who maintain good credit scores, organize financial documents, and present clear business plans significantly improve their chances of securing funding. By choosing the right lender and demonstrating reliable revenue, businesses can access the capital needed to grow and expand their operations successfully.