When people need extra money for emergencies, large purchases, or debt consolidation, two of the most common options are personal loans and credit cards. Both provide access to borrowed money, but they work differently and have different costs, repayment structures, and financial impacts.

Understanding the differences between personal loans and credit cards helps borrowers choose the most suitable option for managing debt and improving financial stability.

What Is a Personal Loan

A personal loan is a fixed amount of money borrowed from a bank, credit union, or online lender. The borrower receives the entire loan amount upfront and repays it through fixed monthly payments over a specific period.

Personal loans typically have repayment terms ranging from one to five years, although some lenders offer longer periods.

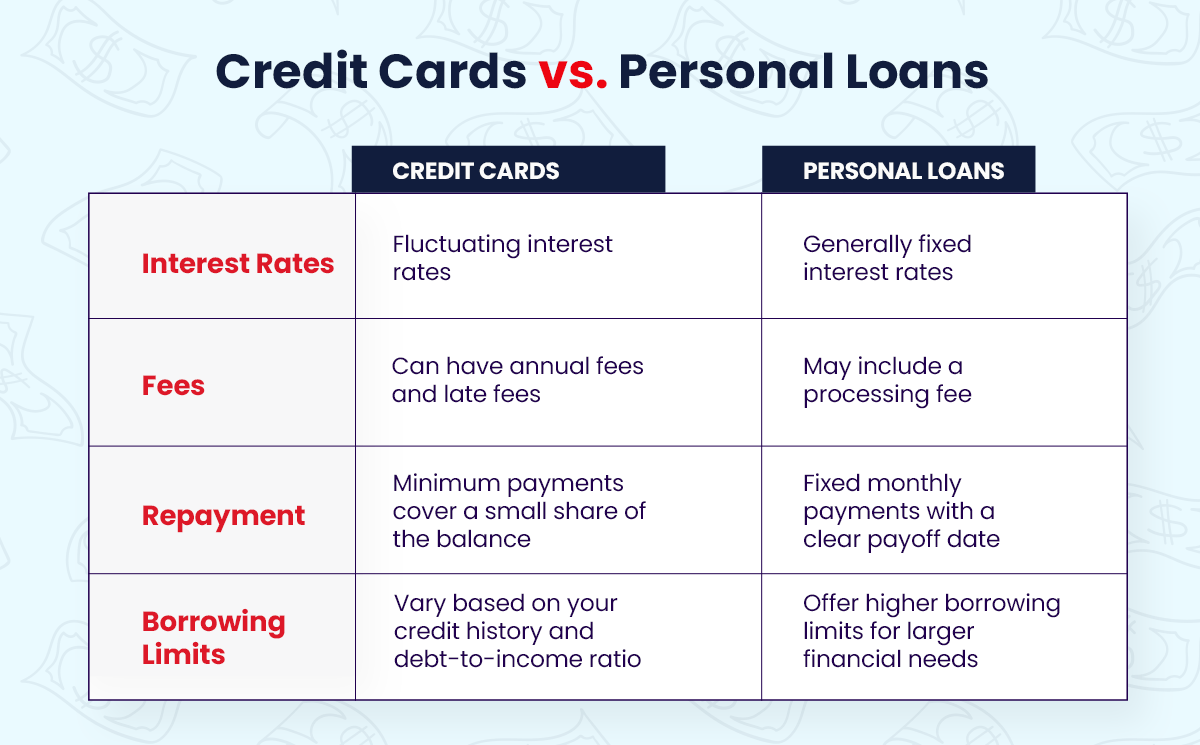

Interest rates for personal loans are usually fixed, meaning the monthly payment amount remains consistent throughout the loan term. This makes budgeting easier for borrowers who prefer predictable payments.

Personal loans are commonly used for debt consolidation, home improvements, medical expenses, and large purchases.

What Is a Credit Card

A credit card provides a revolving line of credit that allows users to borrow money repeatedly up to a set credit limit. Instead of receiving a lump sum of money, cardholders can make purchases or withdraw cash as needed.

Credit cards require a minimum monthly payment, but users can carry a balance from month to month. Interest is charged on any unpaid balance.

Many credit cards also offer reward programs such as cashback, travel points, or purchase protection benefits.

Credit cards are commonly used for everyday expenses, online purchases, and short-term borrowing needs.

Key Differences Between Personal Loans and Credit Cards

One major difference between these two financial products is how the money is distributed. Personal loans provide a lump sum that must be repaid through structured monthly installments. Credit cards allow flexible borrowing as long as the user stays within the credit limit.

Interest rates also differ significantly. Personal loans generally have lower interest rates compared to credit cards, especially for borrowers with strong credit scores.

Credit cards often have higher annual percentage rates, which can lead to large interest charges if balances are not paid in full.

Repayment structure is another key difference. Personal loans have fixed repayment schedules, while credit cards offer flexible repayment options.

When a Personal Loan Is the Better Option

Personal loans are often a better option for larger expenses that require structured repayment. Because personal loans usually offer lower interest rates than credit cards, they can reduce the total cost of borrowing.

Debt consolidation is one of the most common uses for personal loans. Borrowers can combine multiple credit card balances into one loan with a lower interest rate and a single monthly payment.

Personal loans also help borrowers avoid the temptation of repeatedly using credit, which can happen with revolving credit cards.

When a Credit Card Is the Better Option

Credit cards are better suited for smaller purchases and short-term borrowing. Many credit cards offer a grace period during which no interest is charged if the balance is paid in full each month.

Credit cards are also convenient for everyday spending and online purchases because they provide immediate access to funds.

Reward programs offered by credit cards can provide additional benefits such as cashback, travel points, and purchase protections.

For disciplined users who pay their balance in full every month, credit cards can be a cost-effective financial tool.

Impact on Credit Score

Both personal loans and credit cards affect credit scores in different ways. Responsible management of either credit product can help improve credit ratings.

Personal loans contribute to the credit mix component of a credit score by adding installment debt to the borrower’s credit profile.

Credit cards influence the credit utilization ratio, which measures how much credit is being used compared to the total available credit.

Maintaining low credit utilization and making payments on time helps improve overall credit scores.

Interest Rates and Fees

Interest rates are a critical factor when comparing personal loans and credit cards. Personal loans usually offer lower interest rates because they are structured installment loans.

Credit cards often have higher interest rates, especially for borrowers with average or poor credit scores.

Borrowers should also consider additional fees such as annual fees, balance transfer fees, late payment penalties, and cash advance charges when evaluating credit card options.

Choosing the Right Option for Your Situation

Selecting between a personal loan and a credit card depends on the financial needs of the borrower.

If the goal is to finance a large expense or consolidate multiple debts, a personal loan may be the better option due to lower interest rates and structured repayment.

If the need is for short-term borrowing or everyday spending, a credit card may provide greater flexibility and convenience.

Borrowers should compare interest rates, repayment terms, and potential fees before making a final decision.

Tips for Managing Debt Responsibly

Regardless of which borrowing option is chosen, responsible debt management is essential. Making payments on time helps avoid late fees and protects credit scores.

Borrowers should also avoid borrowing more money than they can comfortably repay.

Creating a monthly budget and monitoring spending habits can help maintain financial stability and reduce the risk of excessive debt.

Personal loans and credit cards both offer useful financial solutions when used responsibly. Personal loans provide structured repayment and lower interest rates for larger expenses, while credit cards offer flexible borrowing and reward benefits for everyday purchases. By understanding the advantages and limitations of each option, borrowers can choose the financial tool that best supports their financial goals and debt management strategies.